Security Equity Partners (SEP)

To set up SEP you must have Credit Reports enabled. If you do not have it enabled, you may call our support line and we can turn this feature on for you.

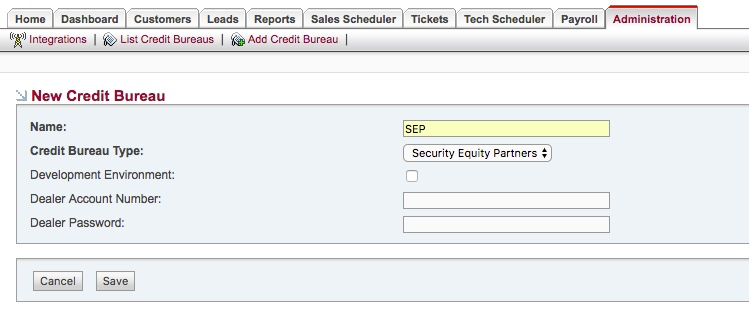

Once Credit Bureaus are enabled you will need to create a new Credit Bureau and input the correct credential information from SEP. This can be found if you navigate to the Administration Tab -> Integrations -> Credit Bureaus.

Once enabled assign the appropriate permissions to your user groups for access to credit reports. If you have the permissions to use credit reports you will see the Credit Reports Button on the customer button navigation bar.

![]()

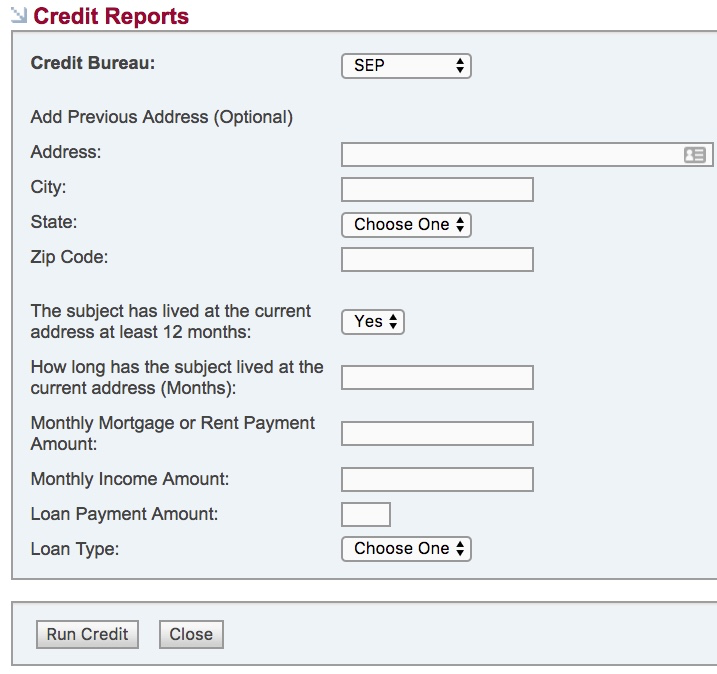

When you open the Credit Reports button, Select SEP from the drop-down menu.

When an application is sent through Security Equity Partners’ integration successfully the application is scored according to the applicant’s credit history. The basic scoring involves 3 factors for an automatic approval at the time of application submission:

1. FICO is 640 or higher

2. Applicant has not filed for bankruptcy in the past 3 years

3. Applicant has not missed a mortgage payment in the past year

If an applicant’s credit history does not pass all three factors, then the application can be scored differently. Not hitting all three factors does not mean they are necessarily declined.

The possible 5 status states when an application is submitted are as follows.

| Status State | Explanation |

|---|---|

| Approved | The applicant passes all 3 scoring factors. |

| Declined | The applicant’s FICO score is 599 or lower or has been in bankruptcy in the past 3 years. |

| Approved – Pending Proof of Home Ownership | The applicant passed the FICO score and bankruptcy check, however, there are no trade lines in the credit history that show he/she is paying on a current mortgage. You or SEP will need to manually verify home ownership from the consumer or business owner. |

| Preapproved for Billing and Servicing (Optional) | Dealer can opt-in for Billing and Servicing through Security Equity Partners. Usually, an application will be declined if the applicant’s FICO score is 599 or lower. A FICO score between 600 – 639 will normally score as a Manual Review. There are three risk levels that a dealer can opt-in for. Risk Level 1: 600 and higher Risk Level 2: 550 and higher Risk Level 3: 500 and higher If the applicant’s FICO score falls within the risk level you have opted in for, then the application will be scored as Preapproved for Billing and Servicing. If you are interested in opting in for billing and servicing or wish to learn more about it, please contact SEP at (888) 501-5612. |

| Manual Review | There are two reasons an application would go into Manual Review. 1. If the applicant’s FICO score is between 600 – 639. 2. If the applicant passed the FICO score and bankruptcy check but has missed 1 or more mortgage payments in the past year the application will go into manual review. |